Traceability of Contractual Processes as a Component of Internal Control and Governance

Introduction

In the context of internal and external audits, contract documentation regularly becomes the focus of in-depth reviews. This is not only due to the legal significance of contracts, but above all to their role as a foundation for business decisions. Contracts define rights, obligations, risks, and financial commitments, often over multiple years. Accordingly, the requirements for their management and documentation are high.

As organizations become more complex, regulation increases, and expectations around corporate governance rise, the focus of audits is shifting. It is no longer sufficient to assess whether a contract exists or what its content is; increasing attention is paid to how it came into existence. Audit-ready contract management today means making decision-making processes traceable, reproducible, and verifiable.

Modern internal control systems (ICS) require companies not only to demonstrate contractual obligations, but also to prove the integrity of the underlying processes. This includes approval workflows, responsibilities, access controls, and compliance with internal policies. Contracts therefore become an audit object that makes process quality, governance maturity, and organizational control capabilities visible.

In this context, the concept of traceability gains particular importance. It describes the ability to transparently present decision-making and processing steps related to contracts at any time — not retrospectively based on memory, but on the basis of systematically documented information.

The Concept of Traceability in the Context of Contract Management

Traceability in contract management refers to the ability to reconstruct the complete lifecycle of a contract in a seamless and structured manner. This goes far beyond simply storing the final version of a contract. Rather, it involves making all relevant process steps and decisions clearly traceable.

This includes, in particular, information on:

- the initiation of the contractual relationship

- the drafting and negotiation phase

- the sequence of changes and versions

- the individuals and roles involved

- approval levels and decision points

- the underlying rationale for decisions

- compliance with internal policies and processes

Traceability is clearly distinct from mere transparency. While transparency means that information is visible, traceability explains why decisions were made and how processes unfolded. A contract may be stored transparently without it being traceable who approved it or why certain changes were made.

For audit purposes, this distinction is essential. Contracts are not viewed as isolated documents, but as the result of structured processes. Audit-ready contract management makes it possible to present these processes consistently even in retrospect, without relying on subjective explanations or subsequent reconstructions.

Traceability as a Component of Governance and the Internal Control System

Traceability is not an end in itself. It is a core element of effective governance structures and an integral part of a functioning internal control system. Governance aims to ensure that business decisions are traceable, compliant, and responsible. Contracts play a key role in this context, as they often form the formal basis for such decisions.

An internal control system that cannot map contractual processes remains limited in its effectiveness. If approvals, responsibilities, and decision paths cannot be demonstrated, gaps arise in management and oversight. For auditors, these gaps indicate structural weaknesses, even when no direct rule violations are present.

Traceability also supports the clear assignment of responsibilities. It creates transparency around which role made which decision and on what basis. In doing so, it strengthens organizational accountability and reduces dependency on individual employees.

Typical Traceability Deficiencies Identified During Audits

In audit practice, auditors frequently identify recurring weaknesses in contract management. These do not necessarily indicate legal deficiencies, but they do reveal shortcomings in process quality and documentation.

The most common findings include:

- the lack of a clearly defined current contract version

- an untraceable chronology of contract changes

- missing or incompletely documented approvals

- decision-making outside formalized processes

- contracts stored across multiple, disconnected systems

- unclear access controls and responsibilities

In many cases, the relevant information exists in principle, but not in a structured or consistent form. Approvals are granted via email, changes agreed verbally, or decisions made informally. For audits, this results in significant additional effort, as information must be consolidated and interpreted after the fact.

This reliance on manual reconstruction reduces the reliability of the documentation. It increases the risk of misinterpretation and significantly prolongs audit processes. In addition, it creates a strong dependency on individual employees whose knowledge is required for reconstruction.

Limitations of Traditional Tools for Contract Storage

In many organizations, contracts are still managed in generic file systems, email inboxes, or spreadsheets. While these tools meet basic requirements for storage and exchange, they are not designed to support audit-ready process documentation.

File systems do not capture decision contexts, approval levels, or responsibilities. Version conflicts easily arise when multiple copies exist in parallel. Changes are difficult to trace chronologically, especially when they occur outside structured processes.

Email-based coordination also quickly reaches its limits. While emails document communication, they do not do so in a way that is systematically analyzable or clearly attributable to a specific contract. Information is lost, remains in personal inboxes, or is not archived consistently.

These structural limitations force organizations to rely on manual consolidation during audits. This weakens the reliability of the documentation and significantly increases the effort required for audit activities.

Audit Focus: Key Areas of Review

When analyzing contractual documentation, auditors look beyond legal content and focus in particular on the quality of the underlying processes. Several key questions are central to this assessment.

Alignment of Internal Policies with Actual Practice

Auditors assess whether documented policies are actually followed. Deviations between formal rules and day-to-day practice indicate weaknesses in the internal control system.

Access Control to Contract Documents

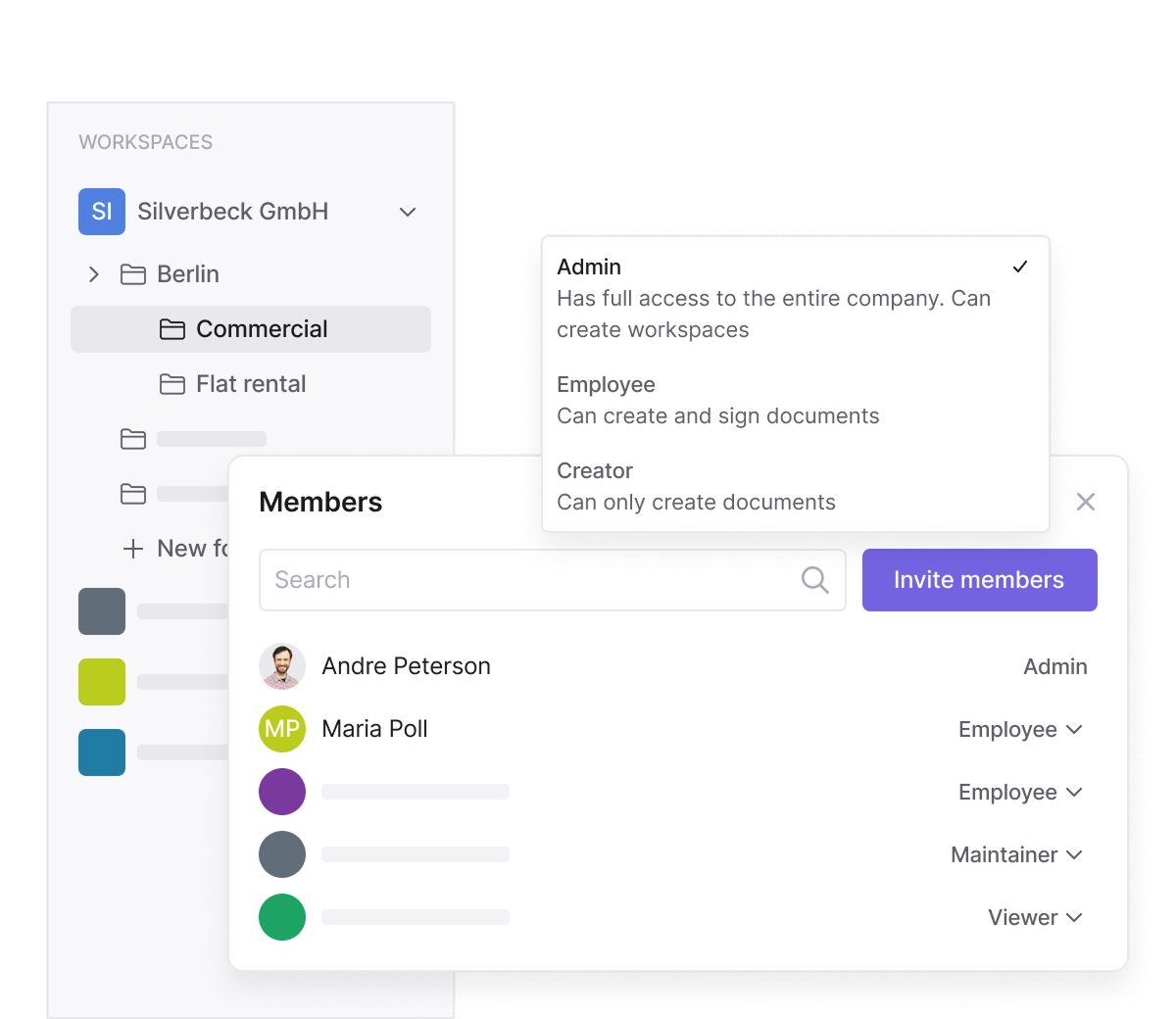

A critical review criterion is who had access to contracts and at what point in time. Missing or unclear access controls make it difficult to assign responsibility and increase security risks.

Documented Approval Processes

Approvals are considered steering management decisions. Auditors expect clear documentation of the roles involved, the timing, and the approval steps.

Documentation of Contract Amendments

Changes must be recorded completely, chronologically, and in a traceable manner. Fragmented documentation of amendments significantly impairs auditability.

Retrospective Review of Decisions

A core objective of audits is the ability to reconstruct decision rationales retrospectively. Subjective explanations cannot replace systematically documented information.

If reliable documentation is missing for any of these aspects, this often results in deeper audits and additional follow-up questions.

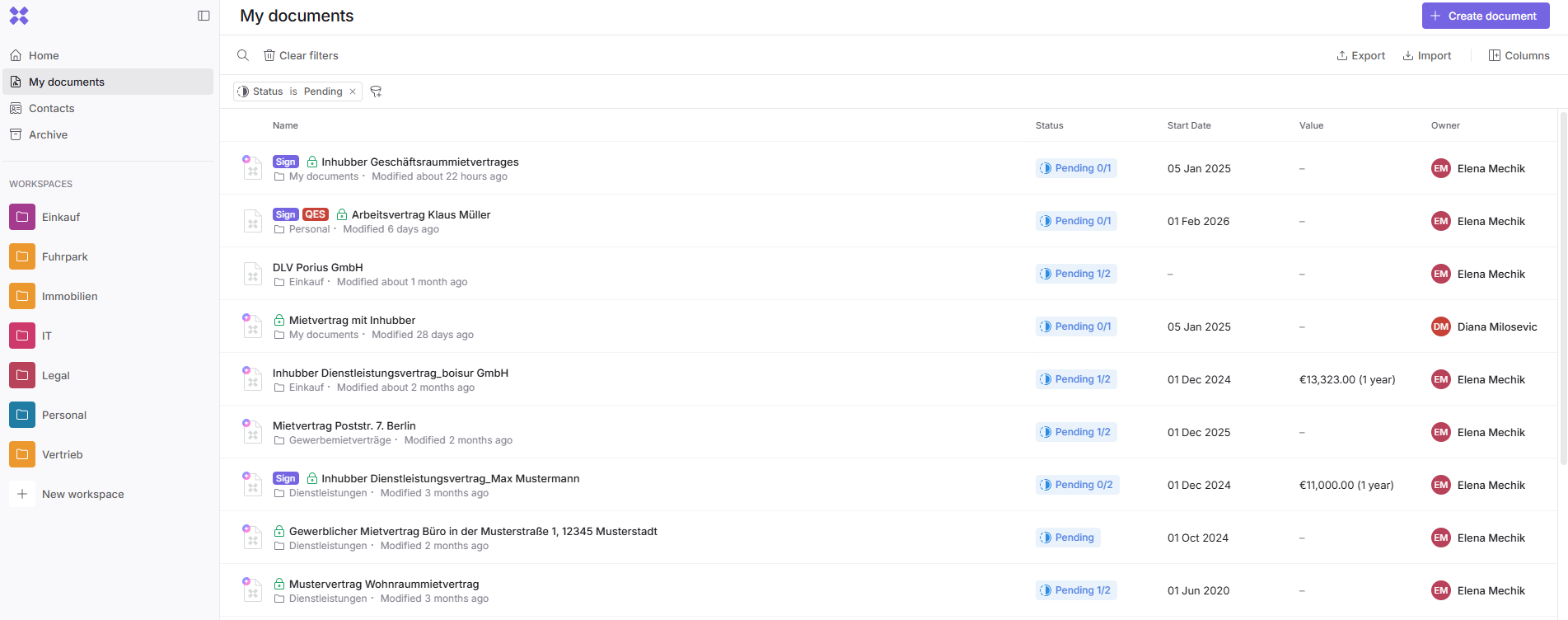

Requirements for an Audit-Ready Contract Management System

From an audit perspective, a contract management system must go far beyond simple document storage. In particular, it should meet the following requirements.

Centralized and Structured Storage

All contracts must be stored in a central, clearly structured environment. This prevents version conflicts and facilitates efficient access during audits.

Controlled and Documented Access Concepts

Access rights must be clearly defined, manageable, and traceably documented. An audit-ready solution enables proof of access at any time.

Automatic Logging of Changes

Changes should be captured at the system level. Automatic logging increases data integrity and prevents subsequent manipulation.

Traceable Approval History

Approvals must be clearly assigned to the respective contract and fully documented.

Reproducibility Without Manual Reconstruction

All relevant information should be directly derivable from the system, without the need for additional manual research.

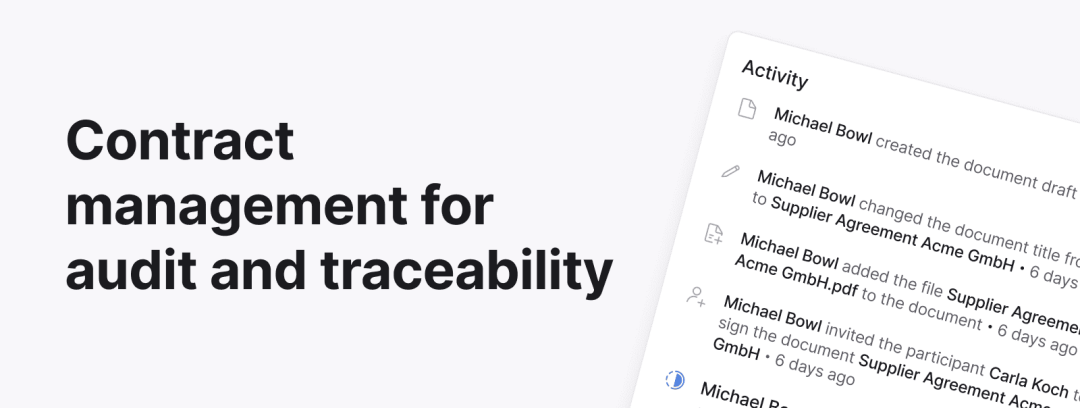

The Role of Digital Contract Management in Ensuring Traceability

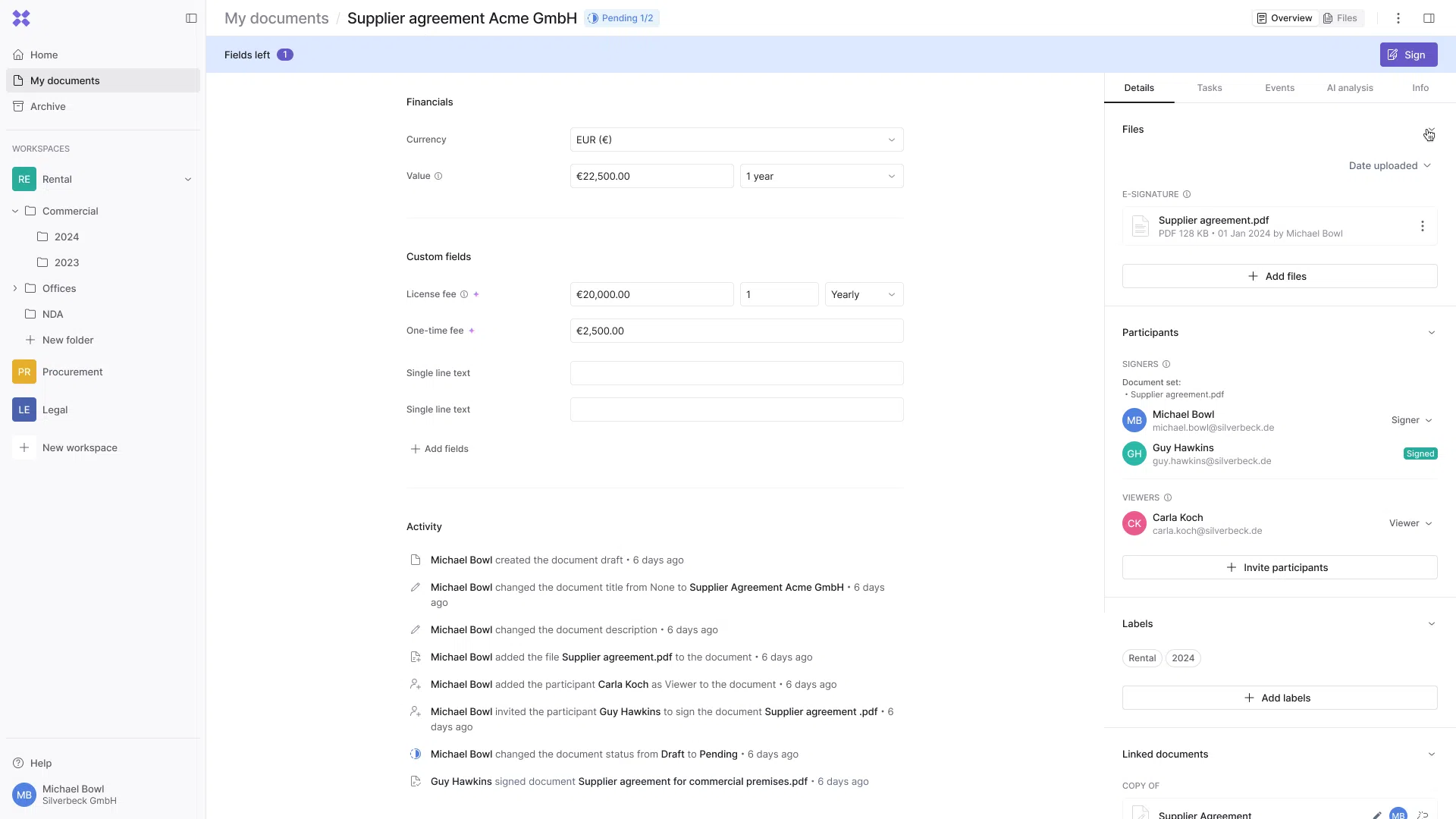

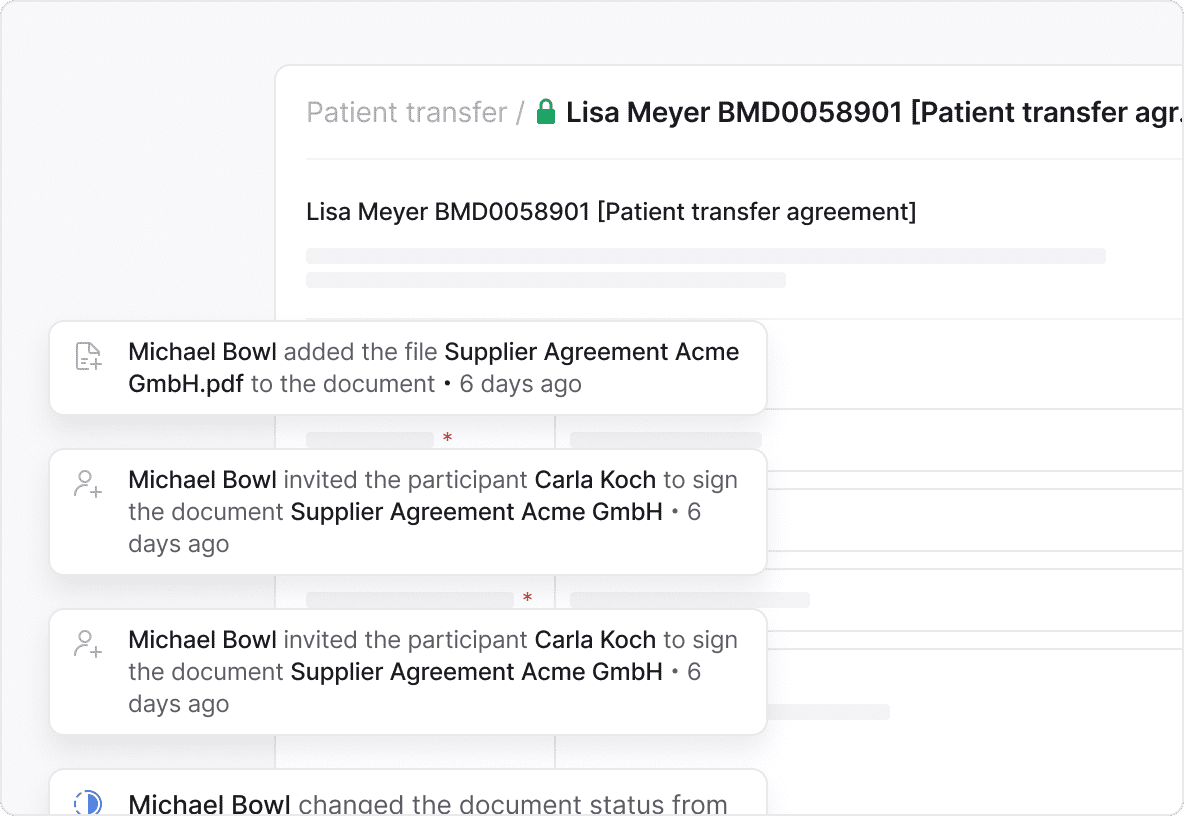

Digital contract management systems connect documents and processes within an integrated environment. Decisions are documented at the moment they are made, changes are automatically versioned, and access is centrally controlled.

Solutions such as Inhubber make it possible to establish traceability as a natural part of day-to-day contract work rather than as a downstream measure during an audit. As a result, audits become more predictable, more efficient, and less disruptive.

Practical Impact for Organizations

Organizations that design their contract management with audit requirements in mind benefit in several areas:

- shorter preparation times for audits

- reduced manual audit effort

- lower operational and regulatory risks

- greater transparency and decision-making certainty

These effects are not achieved through additional controls, but through clear processes and structured documentation.

Traceability from an Audit Perspective: Practical Review and Assessment Insights

From an audit practitioner’s perspective, traceability is not an abstract concept but a concrete assessment criterion that directly affects audit scope, audit depth, and overall audit efficiency. Auditors evaluate not only individual contracts, but in particular an organization’s ability to present processes in a consistent, reproducible, and compliant manner.

In practice, organizations with a high level of traceability move through audits in a far more structured way. Information can be retrieved in a targeted manner, follow-up questions are reduced, and the focus of the audit shifts from information gathering to substantive evaluation. Conversely, deficiencies in traceability often lead to an expansion of the audit scope, additional sampling, and more in-depth analyses.

A key criterion in this context is the system capability of the documentation. Auditors increasingly distinguish between information that is generated and maintained systemically and information that is documented manually or on a situational basis. System-generated evidence is considered more reliable, as it is less susceptible to subsequent adjustments or subjective distortions.

Auditors are particularly critical of processes in which key decisions were made but not clearly documented. This includes informal approvals, verbal agreements, or email-based decision-making without clear attribution to the contract. Even if such approaches appear pragmatic in day-to-day operations, they significantly hinder audit-ready assessment.

Nachvollziehbarkeit als kontinuierlicher Prozess statt punktuelle Prüfungsanforderung

Ein häufiger Trugschluss in Organisationen besteht darin, Nachvollziehbarkeit als reine Anforderung der Revision zu betrachten, die erst im Prüfungsfall relevant wird. In der Praxis erweist sich dieser Ansatz als ineffizient und risikobehaftet. Nachvollziehbarkeit lässt sich nicht kurzfristig herstellen, sondern muss als kontinuierlicher Prozess im operativen Vertragsmanagement verankert sein.

Organisationen, die versuchen, Nachvollziehbarkeit nachträglich herzustellen, sind häufig gezwungen, Informationen aus verschiedenen Quellen zusammenzuführen, Entscheidungen zu rekonstruieren und Verantwortlichkeiten rückwirkend zu klären. Dieser Aufwand bindet Ressourcen, erhöht das Fehlerrisiko und schwächt die Aussagekraft der Dokumentation.

Ein revisionsorientierter Ansatz hingegen integriert Nachvollziehbarkeit in den täglichen Arbeitsablauf. Entscheidungen werden zum Zeitpunkt ihrer Entstehung dokumentiert, Genehmigungen systemisch erfasst und Änderungen automatisch historisiert. Dadurch entsteht eine kontinuierliche Dokumentation, die jederzeit prüfbar ist, ohne zusätzliche manuelle Eingriffe.

Für die Revision bedeutet dies eine erhebliche Entlastung. Prüfungen werden planbarer, da relevante Informationen strukturiert vorliegen. Gleichzeitig steigt die Qualität der Prüfungsergebnisse, da sich Revisoren auf die Bewertung von Prozessen und Risiken konzentrieren können, statt grundlegende Informationen zu sammeln.

Organizational Impact on Specialist Departments and Management

The introduction of traceable contract processes affects more than just audits; it also changes the way specialist departments, management, and control functions work together. Clear documentation reduces room for interpretation, creates a shared understanding of processes, and strengthens the binding nature of decisions.

Specialist departments benefit from clear structures, as responsibilities are unambiguously defined and decision paths are transparent. Inquiries from audit or compliance teams can be answered more quickly because relevant information does not need to be researched individually.

For management, this creates a reliable basis for steering and oversight. Decisions are not only documented, but also traceable in their context. This improves the quality of decision-making and supports consistent governance across different organizational units.

From a risk perspective, traceability also has a positive effect. Deviations from defined processes can be identified early and corrected in a targeted manner before they develop into structural risks. As a result, contract management evolves from an administrative function into an active management instrument.

Digital Contract Management as an Enabler of Audit-Ready Organizations

Digital contract management solutions provide the technical foundation for implementing traceability in a systematic way. They connect documents, processes, and responsibilities within an integrated environment and ensure that relevant information is captured consistently.

Platforms such as Inhubber make it possible to design contract processes so that traceability is not perceived as an additional burden, but as a natural part of daily work. Through structured workflows, automatic logging, and centralized access controls, audit-ready documentation is created without additional manual effort.

In the long term, this contributes to the maturity of the entire organization. Traceable processes strengthen the trust of internal and external stakeholders, reduce audit risks, and support a sustainable governance strategy.

Conclusion

Traceability of contractual processes is not an additional audit requirement, but an indicator of the maturity of the internal control system. Organizations that systematically document and make decision-making processes around contracts reproducible sustainably enhance their governance quality.

Digital contract management provides the foundation for establishing traceability as a standard of daily work and for supporting audits efficiently, in a controlled manner, and without operational friction.